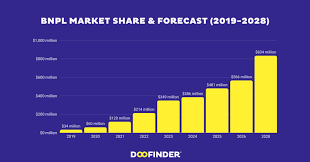

The rapid rise of Buy Now, Pay Later (BNPL) services is transforming the way people shop. This model allows shoppers to split payments into flexible installments. It sounds convenient. However, the booming adoption now raises major financial concerns worldwide. Analysts warn that it could create long-term debt traps if it expands without strong consumer education and fair-use guidelines.

Why Consumers Love BNPL

Many consumers choose BNPL because it offers immediate access to products without full payment. The process appears simple and fast. People also prefer it because there is no heavy paperwork. In addition, younger shoppers embrace it more than traditional finance options. They like digital-first payment flows combined with low friction approval. Therefore, it fits modern spending behavior and lifestyle patterns.

The Hidden Psychological Risk

BNPL feels harmless at first. Yet it changes how people view money. Since payments are delayed, impulse buying rises quickly. Users often assume that future payments will stay manageable. However, when multiple purchases pile up, repayment becomes overwhelming. The concept triggers emotional spending rather than rational budgeting. As a result, even affordable products lead to long-term obligations.

Debt Trouble Builds Quietly

Traditional loans come with strict checks and clear records. BNPL does not always follow the same process. Users can sign up across several platforms while avoiding major friction. Consequently, outstanding debt becomes scattered and difficult to track. Many people forget their total repayment load until deadlines approach. Late fees, roll-over charges and collection pressure can follow. Though it appears friendly, it still carries financial responsibility.

Impact on Global Financial Stability

When large groups rely on delayed repayment, market stability may weaken. Consumer spending grows beyond income capacity. Retailers enjoy short-term gains. Yet the economy receives artificial demand. Over time, unpaid obligations could increase. That drives default trends. When combined with unemployment or economic slowdown, repayment pressure intensifies. Nations with large youth populations may face rapid debt escalation.

Regulation Pressure Will Increase

Authorities are now reviewing BNPL models more seriously. They want clear disclosures, better user protection and transparent repayment structures. Financial education also becomes crucial. People need awareness on budgeting, interest implications and digital responsibility. Without proactive action, the model may repeat past credit bubbles.

What Consumers Should Do Next

People must treat BNPL like real debt. They should track every installment, use budgeting tools and limit non-essential purchases. In addition, they need to avoid stacking multiple BNPL plans across different platforms. Asking a simple question can help: Will future income remain stable enough to handle payments comfortably?

Conclusion

BNPL is not a villain. It offers helpful flexibility when used wisely. However, the expansion now grows faster than financial awareness. Therefore, balance becomes essential. Responsible usage, smarter regulation and better digital money habits will decide its future.